🗝️ Master Key: Who Owns Your Hotel?

A wonky deep dive into the world of hotel ownership structures

Typically, my Master Key series is for paid subscribers. Since this is such an important topic to cover, I decided to gift this one for all subscribers of The Upgrade | Weekly.

For background, I grew up in a hotel family - we owned Outrigger Hotels for 3.5 generations until we sold it in 2016. I now run a personal investment fund that invests in hospitality, venture, and private equity, and hold several LP positions in hotels around the US. I sat on the advisory board of directors for Outrigger for several years and now sit on our larger family’s board, post-sale of the company. From the operational side, I own a travel agency and see the client-facing side of hotel ownership structures frequently. Many people do not understand who owns the hotel they are sleeping in, so I thought this would be a solid place to start.

FYI I learned none of this in business school during my MBA.

-Anne Marie Brown

Who Actually Owns Your Hotel

I was 14 when we broke ground on the Hilton Garden Inn at Denver International Airport. The earth was so frozen that my father couldn’t get the shovel to go in for the photo op. For the next several decades, I attended annual owner meetings at that hotel. I wrote down terms I didn’t understand and looked them up later, too embarrassed to ask what they meant in the room.

In 2021, occupancy hovered around 7%. It was the height of Covid, my dad’s Parkinson’s was testing his mental capacity, and several of the other LP’s (limited partner owners) didn’t want to put up money for a capital call to carry the hotel through more months of shortfall.

My dad asked if I could start leading the LP meetings. If you’ve ever tried to set up an ongoing Zoom meeting with a bunch of men in their 70’s and 80’s, it is not something I would wish on any 35-year-old new mother. Technological difficulties aside, I started finally piecing together the situation we were in.

You may be unfamiliar with how hospitality investment works. I still see people expressing confusion over who actually owns the Four Seasons hotel they want to tweet at furiously. Is the verb still “to Tweet?” is it now “To X at?” If this is wayyyy too much information for you, skip my post. If you are an investment banker, this is not a post for you. You already know this at a level most people will never want to.

But, if you are a casual luxury traveler and want to know about the ownership structure of the places you are staying in, read on.

Here is your hotel investing and ownership guide, level 101

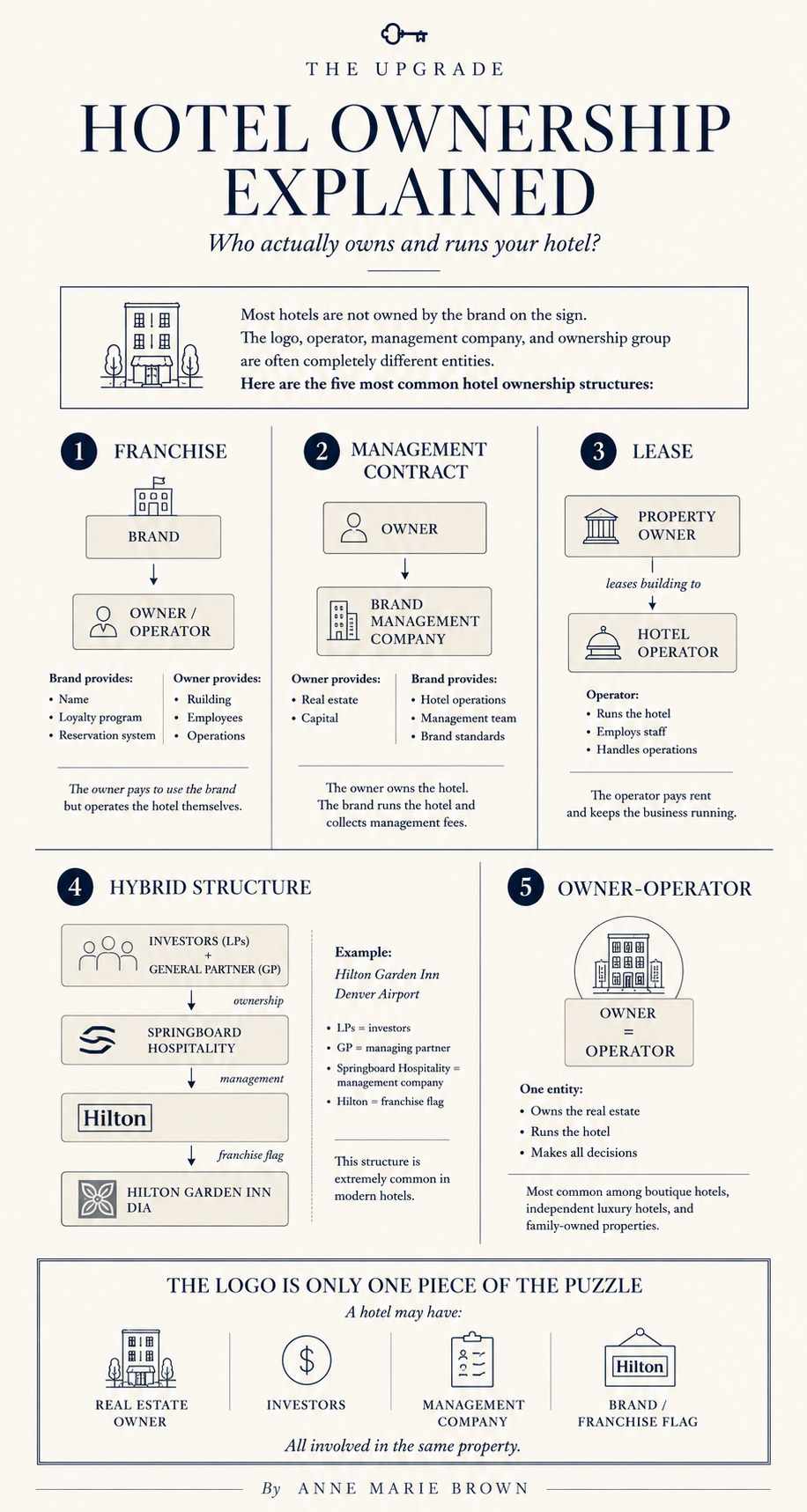

Most hotels operate under one or a mix of these arrangements – franchise, owner/operator, or management. A handful of hotels are owner/operated, but that’s more common at the independent, boutique level.

1) Franchise: Under a franchise deal, an independent owner pays for the right to use the name, the loyalty program, and the reservation system of a brand or “flag.” The owner, or group of owners made up of LPs (limited partners) and GPs (general partners) own and operate the hotel themselves.

2) Management Contract: Under a management contract, the brand runs the hotel instead of the owner/owners. The brand collects additional management fees.

3) Lease: The property owner leases the hotel to a corporation, chain, or operator for a set period. The tenant then runs everything and pays the owner a fixed rent or share of net revenue.

4) Mix of franchise, manager, ownership group of LP/GP. This is what the Hilton Garden Inn at DIA was structured as. We had a group of LPs, my father and I were the GP, we partnered with Springboard Hospitality to manage the property, and then we were flagged as a franchise under Hilton.

5) Owner-operator - The same entity that owns the real estate also operates the hotel. A single family or family office makes all the decisions.

Oetker, Belmond, Airelles are all examples of owner/operator models. Owners typically pour tons of personal capital into a hotel in these models, often without great returns. Other brands that own and operate most of their own properties include Peninsula Hotels, Cheval Blanc, some of the Amans (except what’s owned by the Sacklers).

Our family business, Outrigger, was an owner/operator model. Everything we made went back into the company until we sold it.

Who are these hotel owners?

1) Private Equity Firms — PE firms raise funds with a 7-10 year life, buy underperforming hotels, fix them, and sell them. KSL is an example of a PE firm that invests in hotels.

Private equity firms are among the largest hotel owners in the world, and the ones you are most likely to encounter. In 2024, PE firms represented 30% of all hotel buyers in U.S. deals above $5 million. In 2021, that share was 55%. The pullback since then reflects higher interest rates and a more cautious market, but PE remains a dominant force.

Blackstone is the largest real estate investor in the world and has moved more hotel real estate over the past two decades than any other firm. Its biggest triumph was buying and selling Hilton Hotels, which netted $14 billion when it exited in 2018. Today Blackstone’s hotel strategy centers on buying properties, refurbishing them, and leasing them to luxury operators like Ritz-Carlton, Hilton, and Marriott, where Blackstone is the landlord and the brand runs the hotel. In southern Europe alone, Blackstone committed over 500 million euros in 2024 to hotels in Greece, Spain, Italy, and Portugal, bringing its southern European portfolio to 22,000 hotel rooms across 70 properties.

Starwood Capital Group, run by Barry Sternlicht, is the other name that shapes the industry. Sternlicht created the W Hotels concept, built Starwood Hotels and Resorts into a global brand, sold it to Marriott for $12 billion in 2016, and is now relaunching the Starwood Hotels brand with a new portfolio that includes Baccarat Hotels, 1 Hotels, and Treehouse. Starwood Capital’s funds have invested in approximately 2,600 hotels over the firm’s history.

KSL Capital Partners, based in Denver, is the most hotel-focused of the major PE firms. KSL owns The Grove Park Inn, The Homestead, Barton Creek Resort, and Rancho Las Palmas, and most recently acquired Soneva, the ultra-luxury Maldives and Thailand brand, in May 2025. Unlike Blackstone, which deploys capital across all real estate categories, KSL lives exclusively in travel and leisure, which tends to produce more operationally engaged ownership. KSL is who we sold our family company, Outrigger, to in 2016. They’ve done a solid job since purchasing the company from us.

The critical thing to understand about PE ownership is the time horizon. PE firms optimize for a 5-7 year hold and exit, not for the guest experience as an end in itself. They will invest in a renovation if it drives revenue per available room and justifies a higher sale price. They will cut costs when margins are under pressure. The brand provides operational consistency, but the owner’s financial situation shapes what resources the operator actually has to work with.

2) REITs — Real estate investment trusts are the other major institutional ownership structure. Publicly traded companies required by law to distribute 90% of income to shareholders. REITS invest in stabilized, branded hotels and rarely do turnarounds, unlike Private Equity.

Host Hotels and Resorts is the largest lodging REIT in the world and one of the largest owners of luxury and upper-upscale hotels in the United States. Host owns the real estate; brands like Marriott, Hilton, and Hyatt operate the hotels under management contracts. They acquired Turtle Bay Resort in Hawaii from Blackstone in 2024 for $725 million, which then became The Ritz-Carlton Oahu.

The REIT structure subjects hotel ownership to quarterly earnings pressure in a way that private family ownership or sovereign wealth does not. This shapes renovation decisions, staffing budgets, and capital allocation. The hotel carries a prestigious flag, but the owner is a publicly traded corporation answering to shareholders every 90 days.

3) UHNW Families or Family Offices — The private investment arm of a single ultra-wealthy family (or sometimes couple be in a multi-family office group). Family offices tend to be the most patient owners in the market, holding assets for decades through LLCs.

4) High Net Worth Partnerships — A group of wealthy individuals, usually from the same professional network, pooling capital through a private LLC to buy one asset together. The Hilton Garden Inn at Denver International Airport was an example of this.

5) Sovereign Wealth Funds — Government-controlled investment vehicles from countries like Abu Dhabi or Singapore that take long-horizon LP positions in hotel deals for stable income and capital preservation.

6) Insurance Companies and Pension Funds — Long-duration institutional capital, think CalPERS or MetLife, that wants branded, stabilized assets in gateway cities with no appetite for risk.

7) Hotel Brands — Many brands have gone the way of an “asset light” model in which they don’t own their properties. Marriott, Hilton, and Hyatt spent the last two decades selling off their owned hotels to focus on management and franchise fees. Some examples of owner-operator models include Belmond, and a few Amans.

8) Developer-Operators — Private companies that build and manage their own hotels with no outside investors, eliminating the conflicts that come with management contracts. These are usually small, independent boutique hotels.

9) Opportunity and Distressed Funds — A more aggressive subset of PE that specifically targets hotels in bankruptcy or default, buying at steep discounts and exiting within 3-5 years.

The Role of Banks

Banks do not typically own hotels directly, but they are the invisible layer behind almost every PE and REIT transaction in hospitality. Wells Fargo and Bank of Montreal originated the $553 million financing package for KSL’s 23-property U.S. hotel portfolio in 2025. Goldman Sachs partnered with Starwood Capital on the original Westin acquisition in 1994. Deutsche Bank, JPMorgan, and Citigroup are consistently the debt providers on large hotel portfolio transactions.

It’s helpful to understand the debt structure behind a hotel as well as who owns the equity. PE hotel portfolios funded with floating-rate debt got into serious trouble when interest rates rose after 2022. As of mid-2025, a $265 million loan against a 22-property Starwood Capital hotel portfolio has been shipped to special servicing, with occupancy at 63% and the portfolio generating less than 65% of the revenue needed to cover loan interest. This is the select-service segment of Starwood’s portfolio, not its luxury brands, but it illustrates the leverage risk that comes with PE hotel ownership at any tier.

Understanding the LP and GP Relationship

The people who typically pony up the money are structured as Limited Partners. This is how we usually invest out of our fund, Colorado Ohana Ventures. We have LP positions in a handful of hotels, including:

The Home2 Suites Denver Convention Center

The Santa Monica Proper

Hyatt Boston

Hyatt Irvine

Thompson Denver

Indigo Denver

The Santa Monica Proper

LPs contribute the bulk of the capital and collect returns, but they don’t make operational decisions.

The GP, or General Partner, is usually a developer or hotel investment firm. (We work with Stonebridge, McWhinney, Alpine Investments, and many others). They control the asset, structure the deal, and source the capital (through debt and equity from banks and LPs), in exchange for a smaller equity stake. When the deal performs well, the GP earns a “promote”. A promote is a larger share of the upside designed to reward the party taking on the operational risk.

When a hotel is a franchise, like our little Hilton Garden Inn at Denver International Airport, the hotel brand requires frequent renovations to keep the hotel operating at brand standard. This is a called a “Pip” or Property Improvement Plan. In theory, it’s a good concept and makes sure your Hilton Garden Inn doesn’t smell like mold in the bathroom or have flaking plaster above the bed. However, in reality, we often see brands demanding PIPs just because there’s a new ‘brand standards’ director who wants to make their mark. I’ll never forget the requirement to move our room outlets a few inches up the wall one year. When a hotel switches brands (a reflag), it typically triggers a PIP.

When a hotel’s financial performance falls below the thresholds outlined in its loan documents, the lender can trigger a “cash trap.” The property keeps operating, but distributions to ownership stop until performance recovers. This happened during the pandemic, and many franchise LPs found themselves suddenly facing capital calls to keep their hotels afloat, or fund PIPs during times of low occupancy.

Why Should You Care About Ownership Structure?

If you have no desire to own a small slug of a Hilton Garden Inn at an airport, then most of this terminology will remain meaningless in your life. However, ownership structure can affect your stay, so if anything, it’s good to know why certain hotels, like Airelles and Oetker, deliver a superior guest experience (owner-operator model).

Ownership structure can explain why the “same” brand can feel so different and inconsistent - you are rarely dealing with one single owner. You may be sleeping under a roof owned in part by a financial institution, a family office, a REIT, and a disparate collection of multi-generational individuals.

These owners and the brand may have motivations that are at odds – the LPs want to keep cashflow coming, the PE firm may want to cut costs as much as possible, the brand wants to demand a PIP from the owners to maintain the newest and brightest brand standards.

Owner-operator models like Belmond, Passalacqua, and Oetker can have more control over your inhouse experience. They take, as Nadine at the Stanza put it in her interview with the CEO of Airelles, a “patrimonial view” of ownership.

They are there to steward a legacy asset into the next generation, keeping standards as high as possible. The families that own these properties and companies are often pouring personal wealth into their hotels year after year to fund renovations, pay staff higher than average wages, and maintain their culture of excellence.

At Outrigger, we took great pride in trying to maintain ownership over the experience, and a sense of family across our employee base. We ultimately had to sell to a private equity firm, which I’ll touch on more in depth in a future article for my substack, The Upgrade.

Now that we’ve reviewed ownership structures, here is a Hotel Investor’s Dictionary of

Very Important Terms

A few terms worth knowing:

LP (Limited Partner): Puts in most of the capital, collects returns, or has to pony up capital calls in times of crises. An LP has no or very little say in daily operations. Liability is limited to what they invested. This is us for most of our deals, and the easiest way to enter the world of hospitality.

GP (General Partner): The GP controls the asset, makes operational decisions, typically contributes 5-20% of the equity.

Pref (Preferred Return): The minimum return the LP receives before the GP gets to take home any profit sharing. You’ll typically see the pref expressed as an annual percentage, 8-10% is average. Don’t think you’ll be making a ton of cash on an annual basis investing in hotels – they are a long game. The pref has to be fully satisfied before the waterfall (see below) moves down to the GP’s “promote.” If the deal underperforms and never clears the pref threshold, the GP gets nothing above their invested capital.

Promote (Carried Interest): How developers are paid when deals work. A GP who put in 10% of the equity might walk away with 30% of the gain above the hurdle rate (below).

Hurdle Rate: The performance threshold that has to be cleared before profit-sharing with the GP kicks in.

Waterfall: The order in which cash gets distributed to everyone in the deal. Senior lender gets paid first, then mezzanine debt, then preferred equity, then the LP, then the GP. The GP’s promote sits at the bottom of the waterfall, which means they only get paid when everything above them has already been satisfied. When deals go sideways, the waterfall is why developers sometimes walk away with nothing even on properties that technically stayed solvent.

Cap Rate: Net operating income divided by purchase price. We usually see this as a quick shorthand for comparing hotel values and is our first question when reviewing a pitch. A higher cap rate means more risk, and a lower cap rate means the market sees the asset as stable. As an investor, it may seem obvious but you want to target an underpriced asset, (like during Covid when we bought out some LPs at a discount because they didn’t want to keep paying capital calls), and then sell the hotel for market rates or slightly above when you can stabilize the property.

Comp Set: Short for competitive set, this is the group of hotels a property benchmarks itself against for pricing, occupancy, and performance. A hotel’s comp set is usually 5-8 properties in the same market and category. If the Four Seasons is running 95% occupancy and your hotel is at 70%, that may not be the hotel to compare yourself to because you own a select service property.

Franchise vs. Management Contract: See first section. Under a franchise, the owner runs the hotel and pays for the brand name. Under a management contract, the brand runs everything and the owner(s) collects (or doesn’t collect) the returns.

Key Money: this is cash paid by a brand to an owner in exchange for signing a management or franchise agreement. For example, say you as an ownership group agree to fly the Rosewood flag at your new hotel, so Rosewood gives you upfront cash to lock in the deal. Often, key money with longer terms and harder exit clauses.

Reflag: When a hotel switches brands, like when a Courtyard Marriott becomes an Autograph.

PIP (Property Improvement Plan): The mandatory renovation a brand requires of franchise owners. Can run $15,000 to $75,000+ per room. Annoying and at times arbitrary, but understandable in theory.

Mezzanine Debt / Preferred Equity: Capital that sits between the senior bank loan and the ownership equity. This investment is higher risk, higher return, typically 10-14%

Ground Lease: When the hotel owner doesn’t own the land the building sits on. They lease it, usually from a family trust, municipality, or estate. This is a term to watch for if you’re an LP in a deal where the GP owns the land and their operating company is executing a ground lease. It can feel like double dipping from the GP, and complicates financing significantly.

General Hotel Finance Terms

Revenue, Distribution, Cost Metrics:

RevPAR – Revenue Per Available Room. Also see NRevPAR (Net RevPAR) — RevPAR after distribution costs (OTA commissions, booking fees)

GOPPAR (Gross Operating Profit Per Available Room) — profit, not just revenue, per room

BAR (Best Available Rate) — the lowest publicly available rate on a given night

LOS (Length of Stay) — average nights per booking; hotels use minimum LOS restrictions to manage demand

F&B capture rate — percentage of hotel guests who spend money in the restaurant or bar

GDS (Global Distribution System) — Amadeus, Sabre, Travelport; used by travel agents and corporate bookers

Cost of acquisition — total cost to secure one booking; OTAs typically run 15-25%

CPOR (Cost Per Occupied Room) — total departmental costs divided by rooms sold

FF&E reserve — furniture, fixtures and equipment fund; typically 3-5% of revenue set aside for capital upkeep

Thanks for coming to hospitality investing 101.

For transparency - the investment terms and list of revenue, distribution, and cost metrics were pulled with the help of Claude and Notebook LLM, where we have many of our previous hotel investment subscription documents held. All other writing is fully my own.

Anne Marie Brown, The Upgrade | Weekly

I think you just did a better job then my 4-years of Penn State ;) This only made me want to connect further with you more. One additional distinction - that has blown my mind - especially in the US (Oh did I mention I just worked for an ownership/management group..) the brands aren't typically managing anymore - unless it's high end full service. There are a HUGE amount of 3rd party managers. I tell this to friends all the time who want to get mad at Hilton for a bad stay. The bad stay was not Hilton's 'fault' Hilton is a franchisor. The owner and/or management company are really in charge of the guest experience....

Thank you for sharing. I really enjoyed your piece. I used to be head of PR for Omni Hotels & Resorts. Omni is the owner/operator of almost all its 50+ hotels. Those hotels you mentioned that KSL used to own are now owned by Omni’s parent company TRT Holdings. Omni is the owner operator and brand of Omni Grove Park Inn, Omni Barton Creek and Omni Rancho Las Palmas and Omni Homestead. Omni invested $155M in Homestead’s restoration. Again, your piece is perfect for PRS entering into the hospitality space.